A warning. Not a prediction.

“Tiny bubbles (tiny bubbles)

In the wine (in the wine)

Make me happy (make me happy)

Make me feel fine (make me feel fine)”Leon Pober, popularized by singer Don Ho, “Tiny Bubbles,” 1966

Things could go wrong.

I am talking about the economy and your retirement, not Trump.

It is an enormous relief not to feel responsible for the financial and emotional well-being of my investment clients. I loved my work, but I felt a relentless sense of responsibility. Ten years ago, a week after I retired, I sat at this desk and read the financial news and realized that the weight on my shoulders was gone. I had my own money to consider, but no one else’s. When one retires from Morgan Stanley, as I did, one is forbidden to give investment advice for five years, lest former clients think they are getting advice from a Morgan Stanley agent when they are not.

I am retired, a private citizen. I am free to say that the stock market isn’t cheap and that it gives me the willies.

I feel like we have been in investment crazyland twice before. One crazyland was the internet boom years of the late 1990’s, culminating in March of 2000. And again in 2006-2007 period in mortgage lending when TV ads advertised 110% cash-out financing on new home purchases.

My personal experience in the financial markets is that about every decade it all goes to hell all over again. People chase opportunity and they forget. It doesn’t go to hell from a starting point of discouragement and caution. It goes to hell from a starting point where people all around you got rich, quickly and easily, buying something that seemed to have perfect logic. In the 1990s we knew that the new internet thing would change everything, so buy tech stocks. In the mid 2000s banks saw that mortgage loan packages converted high-yielding mortgages into AAA-rated supposedly risk-free bonds and that they could put generous margin in them. Quick money.

Enthusiasm and optimism worry me.

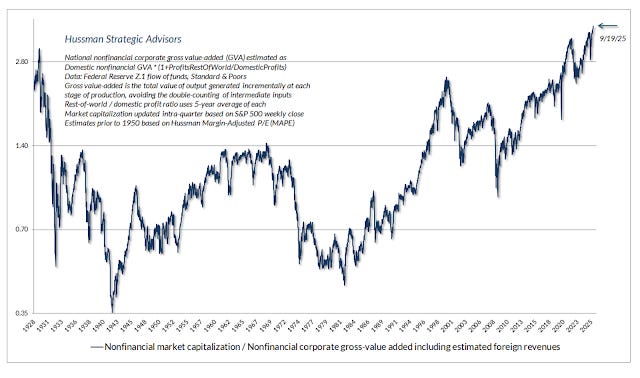

Reading John Hussman’s analysis of the risks to stock investors will give you the willies. He says the stock market is at the highest, craziest valuation in history. Higher than 1929. Higher than March 2000. He anticipates the market return over the next decade to be negative. How negative? Six percent a year compounded negative. Whew!

Notice that we are far in excess of the valuations at the beginning of the chart in 1929, and higher than the 2000 peak. Notice one more thing, that big M-shaped price line toward the right, showing the price from 1994 to 2008. I lived through that one. People who bought stocks in what turns out to be the market peak in the leadup to the year-2000 top did not get even for over 15 years. It is a long time to be under water. If one was age 30 and saving through the period, it was an opportunity. For someone in her 60s, counting on investment earnings to fund a retirement lifestyle, it was life-changing.

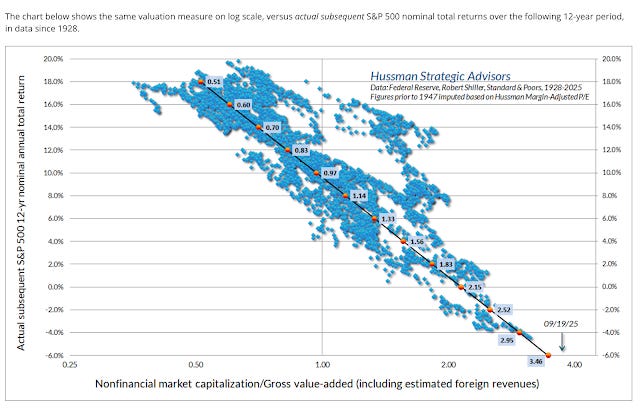

This scattergram of historical valuations and returns puts the current status at the bottom end of expected returns. The stock market is not cheap.

But relax. John Hussman has been worrying for a long time and he has been wrong, even as markets have gone up, notwithstanding his warnings. He is a worrywart.

In the long run, I expect the U.S. economy, and therefore the stock market, to be OK. People adjust to circumstances. People are inventive and ambitious, and life will go on. There are lots of catalysts and tripwires for the economy but eventually things will resolve themselves. Just have patience; buy and hold and keep adding money.

The problem is that no one lives a life “in the long run.” We don’t get “average.” We get the hand we are dealt at that moment of our life.

The “Magnificent Seven” stocks trade at some 33 times earnings -- high -- but maybe well worth it because their growth potential is so high. Investors think these stocks are special. That is what people think at points of enthusiasm. The rest of the 493 stocks are high but not crazy-high, with a PE ratio nearer 23. Average is about 16. Stock market prices embed a lot of optimism.

Ignore me. I suspect I am just an old fart full of the worries and cautions that arise from looking backward too much. It is easier for me to see past hazards than new opportunities, because I won’t be around for much of the wonderful potential world of the next half century.

I don’t know if things will go wrong. I am not predicting. But this I know: Sometimes things go wrong.

It’s hard to make predictions, especially about the future. But I predict money will continue to come and go. In fact, it’s getting past time for some of it to go back from the haves to the have nots.

In a way, this is about Trump. Isn’t his on-off-on again tariff craziness about manipulating the stock market so he can take advantage when it drops and rises?

I have a series of buy orders for index funds, laddering limits down from a 15% correction on down to an average-bear 33% decline, and I have been readjusting during the last few weeks as the market made new tops. Do I want to own a basket of stocks after they crash? I suppose I will have buyer's remorse, especially if the market tanks further. "Nobody rings a bell at the bottom" was the mantra long ago, I recall.

I never cease to be amazed at how the market refuses to do what I want it to do. It's been this way ever since the Dow first went over 1,000 and I was certain it was too frothy.