Risks to watch out for

Today's post isn't a prediction of doom. It is a warning about risks.

A recession or banking crisis ends presidencies.

The reality of politics is that sometimes there are great waves of sentiment. Economic problems in an election year mean that even popular politicians get washed out of office.

Democrats have positives going into 2024. Republicans are catering to their extremes on abortion, which scares people. The route to the GOP presidential nomination appears to be by echoing and amplifying Trump, and Trump scares people. Unemployment is low. The Gross Domestic Product has returned to the pre-Covid trend line and is bigger than ever. Inflation is coming down. Gasoline prices are down. Democratic policies like expanded health care and rebuilding infrastructure are popular, and Republicans are positioned against them. But none of that will matter if there is a banking crisis or recession in the months leading up to the 2024 election.

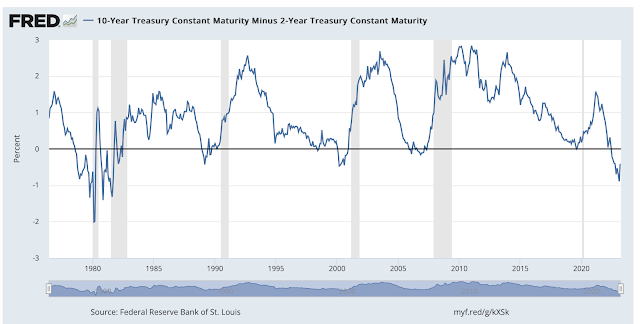

This chart is issued by St. Louis Fed. The yield on the 2-year Treasury rate is subtracted from the 10-year rate. The yield curve is negative when the rate dips below the horizontal line at zero. It is negative again.

See the relation to presidential losses? Carter in 1980. George H.W. Bush in 1992. Al Gore underperformed in 2000. Republican wipeout in 2008.

Will we get a recession this time? No one knows. But it's a risk.

The yield curve is negative because the Fed is trying to slow down the economy to end post-Covid inflation. It is intentional. Sometimes the economy is disrupted by accident. Covid was an accident. A banking crisis is an accident.

No one quite understood how vulnerable the Silicon Valley Bank was to a run. The bank was forced to sell at a loss the low-interest-bearing bonds they had in their portfolio of assets. The depositors didn't know there was a problem. The regulators and credit rating agencies suspected a problem, but didn't think it critical. Even the bank managers didn't know until it was too late.

Other American banks have the same problem. Loans made back when interest rates were much lower than they are today are worth less than face value. The Fed, the FDIC, and Treasury all say they they are on top of this problem.

But I was a Financial Advisor back in 2007-2008, and those same people told the public they were on top of that problem, too. They sounded confident and reassuring. We know there are questionable mortgage loans, they said, but because we know the problem, we are solving the problem. Bank reserves are ample.

My employer at the time, Citigroup, told Advisors like me that there would be a lot of bank failures, but we, Citigroup, were ahead of the curve. We are big and we have reserves, they said. We have it covered, they said. Bank leaders told Advisors that Citigroup would profit by picking up failed wreckage of other banks, and do it on the cheap.

Shortly, Citigroup was wreckage. Government didn't "have it covered," nor did Citigroup. In a contagion the backstop insurance one has in place is worthless. One's supposed assets aren't assets, because there is no one to sell them to. Your counter-parties are desperate to sell, not buy. Bank contagions are like wave elections. Even the strongest are washed away.

Will that happen this time? No one knows. But it is a risk.

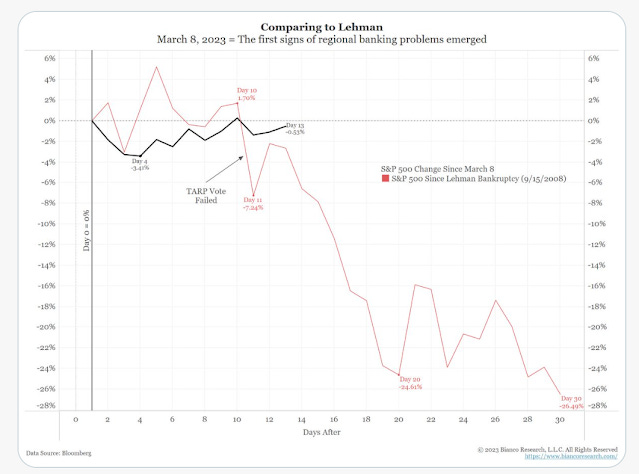

Sometimes what seems like the end of a crisis is really just the beginning. Here is where we are today, overlaid by the timeline of the Lehman Brothers crisis. This wasn't the end. It was the second inning.

I am not predicting doom. My intention is to warn readers about risks. Spokespeople for trustworthy institutions--the Fed, the FDIC, Treasury--have a powerful incentive to reassure the public. If people get spooked, they become a stampede. If everyone stays calm and markets function well, then banks can sell out of their underwater loans or they will mature at par. That works until it doesn't, and if it doesn't, all hell breaks loose.

And in that case the public will vote for whoever the Republican candidates are.

Nah, don’t think so.