Globalization's End.

End of an era.

You don't know the tide has turned until you look back and see that it already turned.

"Let's ride it up and sell it when it starts to go down."

I heard that sentence often from new clients during my career as a financial advisor. They would tell me to buy something that caught their interest because it had gone up in price. My clients were intelligent, reasonable people and their request sounded reasonable to them. However, there is an enormous contradiction embedded in the sentence. The going down trend is only evident after it has gone down. At the start the trend is still going up.

Lawrence Fink is the CEO of BlackRock, the largest asset manager in the world. His letter to shareholders caught attention. He said it was the end of an era for globalization. Several things happened simultaneously which reveal an enormous weakness in this sixty-year trend toward globalization in the post-WWII world. The world rode the trend up to the point where its fragility is too much to bear. COVID, war, and even a container ship stuck in the Suez canal exposed how delicate the world economy had become.

Businesses seek efficiency, and supposedly we all profit from the growing prosperity that results. Businesses want the lowest price from suppliers and they don't want the burden of inventory. Supply chains were getting so efficient and reliable that business sent the manufacture of parts, and sometimes final assembly, to Asia. Shipping by container is dependable and cheaper than paying American labor. Just-in-time inventory is efficient: Why pay to own and warehouse inventory when container ships and trucks could have goods ready when you chose. Capital, too, is globalized. Why invest in good opportunities in the USA when there are spectacular ones overseas, where companies have cheaper labor, where there is no EPA, no OSHA, no labor unions?

The transformation of global capital had consequences. Inflation declined and then disappeared. Business and final consumers had market power to insist on the cheapest and most efficient supplier. Walmart was notorious for insisting on the cheapest supplier, and then, when the supplier had made the factory investments to supply at the cheapest possible price, demand that they supply it yet more cheaply. Otherwise, they would shop for someone new, leaving stranded that company's investment made to supply Walmart. Walmart customers loved that. It was hardball capitalism. Customers, too, demand cheap.

Francis Fukuyama wrote the highly praised book, The End of History. It describes the final triumph of modern global interconnection and efficiency. We had largely solved the problem of war and conflict. We could get along in healthy, efficient prosperity. Countries would become liberal democracies because everybody's needs were being served. Things were so cheap at Walmart.

We know better now.

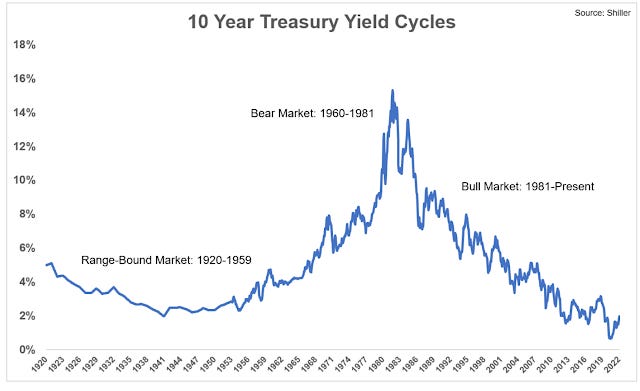

Fink may be right and now we are experiencing now the reversal of great multi-year trends. Treasury rates have moved up--but it may just be a jiggle in a trend that will continue indefinitely. We don't know yet.

Mortgage rates have turned faster than treasury rates. Were you waiting to sell your house until home prices stopped going up? That nice young couple who might have paid top dollar a few months ago, made possible by low principal and interest payments, may be rethinking their options. Or this, too, might just be a jiggle in a long-term trend of low interest rates.

The world is not as safe a place to live, to invest, to manufacture, as we had gotten accustomed. There has been a change in the trend of our thinking. That change has taken place. The invasion of Ukraine reminds us that wars and revolutions are not reserved for skirmishes between small countries.

The trend of putting a company's critical manufacturing offshore is now firmly understood to be a high-risk decision--perhaps a firing offense for a V.P. of manufacturing. American auto manufacturers cannot build cars because computer chips aren't being made and delivered from factories in South Korea and Taiwan. Customers are paying above sticker price. People have money and they want things that aren't being made. So we have inflation.

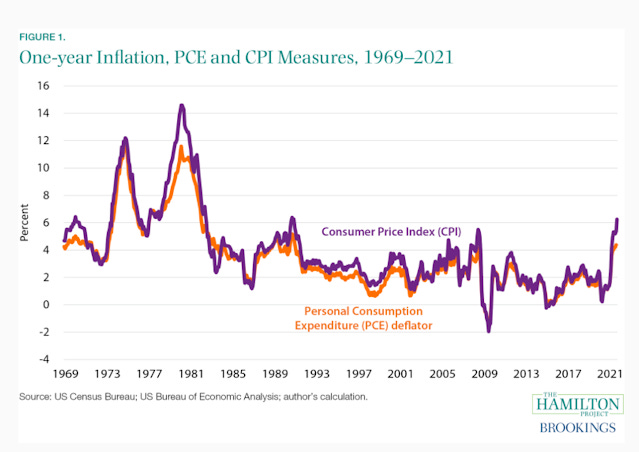

Maybe inflation, too, is a blip, but it doesn't feel insignificant or harmless. I paid $70 to fill up the tank of my Honda Ridgeline pickup truck. With inflation at 6%, while the cash in my accounts pays zero, I feel like I am falling behind, because I am. There is a mismatch between bond yields and inflation. The mismatch is what I would expect when the big trends turn. Eventually treasury rates, inflation rates, and mortgage rates will come into sync. Probably. But not now.

Everything may be changing.

Happy that I sold my original house last summer, phew! Sold if for 40k more than I was expecting, too.