Dividing by zero

Dividing by zero

Very low interest rates make people crazy.

It is dangerous to participate in an economy where people are doing crazy things.

It is even more dangerous when the crazy period ends. Interest rates are going up.

People say I am a "doom scroller." This blog sends up warnings, most often to Democrats, who I worry are doing self-destructive things, by accident and foolishness. Democrats mostly live in urban, multicultural enclaves of educated people and they are certain they are morally and practically correct. I am part of that cohort but think I recognize better than my friends that much of what we think and favor is politically unpopular, and we aren't making it popular. The voters are warning us, if we will listen. How else could someone so flagrantly unfit and dangerous as Trump get the support of about half of America?

I feel like a killjoy. I sometimes feel like an unpopular designated driver--only I am sitting in the passenger seat. Politics is crazy, and so is the economy. So I am doing more doom scrolling today.

The Federal Reserve has made extraordinarily low interest rates a matter of policy for over a decade. They created the crazy. Since the GOP largely blocked infrastructure fiscal stimulus to get us out of the Great Financial Crisis of 2008-2009 the Fed compensated with huge monetary stimulus. They recapitalized banks and other businesses that acted like banks (AIG, General Electric, brokerages), they bought distressed mortgage and corporate bonds, and they made interest rates near zero. It gave investors the confidence that when problems happened, the Fed safety-net would protect them.

It also meant borrowing was very inexpensive. For over a decade the return on bank deposits held by savers are less than zero. Inflation was low--about 2%--so people lost money by holding cash. Currently, inflation worldwide is about 8%--and returns on safe, liquid savings are still about zero. The Fed, at long last, is responding by raising borrowing rates, but even now with "sky high" mortgage rates at 6%--up from 3% a year ago, with inflation at 8%-- a borrower is paid to borrow money.

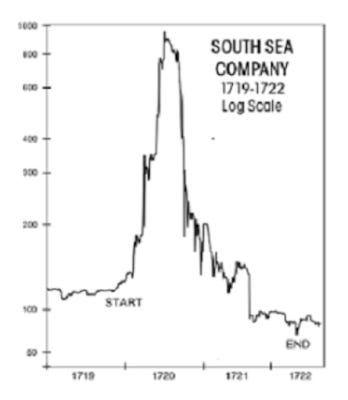

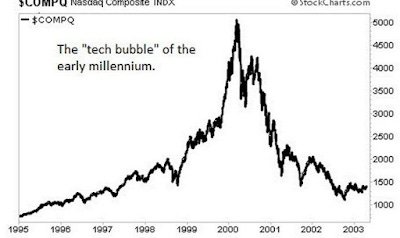

That has the same effect on the economy as dividing by zero has on a math problem. It makes a crazy result. Investors range between restless and crazy if they see themselves doomed to lose money doing something "safe and prudent." A great many people need "safe and prudent" investments. It isn't available, so they seek yield where they can get it, in risky investments. Stock prices reflect that desperation. The financial world did what it does. It creates products to feed investor appetites. Remember leveraged buy-outs and junk bonds in the 1980s? Remember internet IPOs? Remember "derivatives"? Remember collateralized mortgage bonds?

Today we have Non Fungible Token investments in what are essentially digital baseball cards, investment pools in art, and crypto currencies. None of these are investments in businesses that create products or services which have present and future earnings to distribute. Investors are buying a static physical or digital "asset" with a price, hoping someone else will pay a higher price. Price isn't value.

Investors are acting crazy because the free borrowed money is crazy. I have seen these things unwind, past and again now. Market prices for stocks--especially technology stocks, are down sharply this year, as are NFTs and cryptocurrencies. Remember what happened to internet stocks in 2002. Even the lucky companies that survived did so after shedding 90% of their price. This may not be the bottom.

Maybe we could have a huge bear market without a recession and high unemployment. Boomers are retiring. Help-wanted signs are everywhere. The Fed raising the price of borrowing theoretically could reduce foolish speculation without crashing the economy and employment. The economy might cool off by making the rich less rich, not by taking jobs from the poor to make them even more poor. But that is not how it worked out in the past. Crashes end up hurting everyone.

My readers skew older and prosperous. So I send up a warning. People who look at their investment accounts and assume it represents real, solid, reliable value, may be caught up in the crazy, even if they don't want to be and even if they don't own NFTs and cryptocurrencies. Those account numbers may only represent current price, and a false one at that.

Be careful. We are in transition.